Page 71 - Azerbaijan State University of Economics

P. 71

Murad Yusifov: Modelling the inflationary processes and forecasting:an application of ARIMA,

SARIMA models

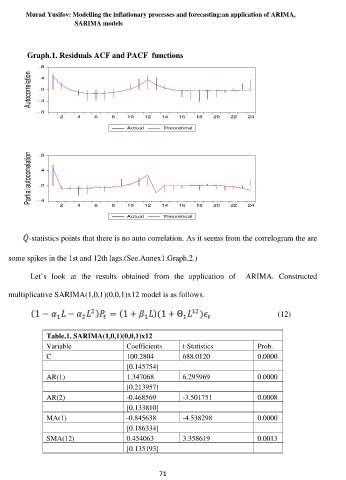

Graph.1. Residuals ACF and PACF functions

.8

Autocorrelation -.4

.4

.0

-.8

2 4 6 8 10 12 14 16 18 20 22 24

Actual Theoretical

Partial autocorrelation .8

.4

.0

-.4

2 4 6 8 10 12 14 16 18 20 22 24

Actual Theoretical

-statistics points that there is no auto correlation. As it seems from the correlogram the are

some spikes in the 1st and 12th lags.(See.Annex1.Graph.2.)

Let`s look at the results obtained from the application of ARIMA. Constructed

multiplicative SARIMA(1,0,1)(0,0,1)x12 model is as follows.

(12)

Table.1. SARIMA(1,0,1)(0,0,1)x12

Variable Coefficients t-Statistics Prob.

C 100.2804 688.0120 0.0000

[0.145754]

AR(1) 1.347068 6.295969 0.0000

[0.213957]

AR(2) -0.468569 -3.501751 0.0008

[0.133810]

MA(1) -0.845638 -4.538298 0.0000

[0.186334]

SMA(12) 0.454063 3.358619 0.0013

[0.135193]

71