Page 30 - Azerbaijan State University of Economics

P. 30

THE JOURNAL OF ECONOMIC SCIENCES: THEORY AND PRACTICE, V.83, # 1, 2026, pp. 20-39

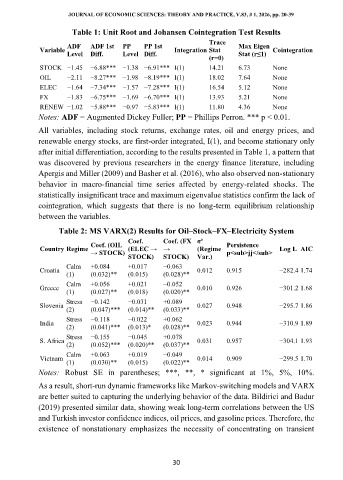

Table 1: Unit Root and Johansen Cointegration Test Results

Trace

ADF ADF 1st PP PP 1st Max Eigen

Variable Integration Stat Cointegration

Level Diff. Level Diff. Stat (r≤1)

(r=0)

STOCK −1.45 −6.88*** −1.38 −6.91*** I(1) 14.21 6.73 None

OIL −2.11 −8.27*** −1.98 −8.19*** I(1) 18.02 7.64 None

ELEC −1.64 −7.34*** −1.57 −7.28*** I(1) 16.54 5.12 None

FX −1.83 −6.75*** −1.69 −6.70*** I(1) 13.93 5.21 None

RENEW −1.02 −5.88*** −0.97 −5.83*** I(1) 11.80 4.36 None

Notes: ADF = Augmented Dickey Fuller; PP = Phillips Perron. *** p < 0.01.

All variables, including stock returns, exchange rates, oil and energy prices, and

renewable energy stocks, are first-order integrated, I(1), and become stationary only

after initial differentiation, according to the results presented in Table 1, a pattern that

was discovered by previous researchers in the energy finance literature, including

Apergis and Miller (2009) and Basher et al. (2016), who also observed non-stationary

behavior in macro-financial time series affected by energy-related shocks. The

statistically insignificant trace and maximum eigenvalue statistics confirm the lack of

cointegration, which suggests that there is no long-term equilibrium relationship

between the variables.

Table 2: MS VARX(2) Results for Oil–Stock–FX–Electricity System

Coef. Coef. (FX σ²

Coef. (OIL Persistence

Country Regime (ELEC → → (Regime Log L AIC

→ STOCK) p<sub>jj</sub>

STOCK) STOCK) Var.)

Calm +0.084 +0.017 −0.063

Croatia 0.012 0.915 −282.4 1.74

(1) (0.032)** (0.015) (0.028)**

Calm +0.056 +0.021 −0.052

Greece 0.010 0.926 −301.2 1.68

(1) (0.027)** (0.018) (0.020)**

Stress −0.142 −0.031 +0.089

Slovenia 0.027 0.948 −295.7 1.86

(2) (0.047)*** (0.014)** (0.033)**

Stress −0.118 −0.022 +0.062

India 0.023 0.944 −310.9 1.89

(2) (0.041)*** (0.013)* (0.028)**

Stress −0.155 −0.045 +0.078

S. Africa 0.031 0.957 −304.1 1.93

(2) (0.052)*** (0.020)** (0.037)**

Calm +0.063 +0.019 −0.049

Vietnam 0.014 0.909 −299.5 1.70

(1) (0.030)** (0.015) (0.022)**

Notes: Robust SE in parentheses; ***, **, * significant at 1%, 5%, 10%.

As a result, short-run dynamic frameworks like Markov-switching models and VARX

are better suited to capturing the underlying behavior of the data. Bildirici and Badur

(2019) presented similar data, showing weak long-term correlations between the US

and Turkish investor confidence indices, oil prices, and gasoline prices. Therefore, the

existence of nonstationary emphasizes the necessity of concentrating on transient

30